Expertise

Blog

Raising the Bar: What a Higher CTR Threshold in the U.S. Could Mean for FCC

AMER

AML

Compliance

Regulatory

A Half-Century Later - Time to Revisit the $10,000 Rule?

For the first time in over 50 years, U.S. lawmakers are proposing to raise one of the cornerstones of the country’s anti-money-laundering (AML) framework - the Currency Transaction Report (CTR) threshold.

A bipartisan Senate bill introduced last month would increase the cash-transaction reporting threshold from $10,000 to $30,000 and, crucially, index it to inflation every five years - a change that would automatically keep it aligned with economic reality.

Supporters frame the move as long-overdue modernization of an outdated limit, while critics warn it could weaken transparency. As debate intensifies, the proposal has ignited fresh discussion across the financial crime compliance (FCC) community. Below, we explore both sides of the argument and unpack what’s at stake.

The Backbone of AML: Understanding CTRs and Their Role

The Bank Secrecy Act has required financial institutions to report any cash transactions exceeding $10,000 within a single business day by filing a Currency Transaction Report (CTR) for over 50 years.

Since 1990, these filings have flowed through the Financial Crimes Enforcement Network (FinCEN), enabling authorities to map and analyse large cash movements that might signal illicit activity - from money laundering to tax evasion.

Alongside CTRs sit Suspicious Activity Reports (SARs) - more discretionary filings that flag behavior the institution deems suspicious. Together, CTRs and SARs form the dual pillars of AML reporting in the U.S. Yet while financial crime, technology, and inflation have evolved dramatically since 1970, the $10,000 threshold has never been adjusted.

In today’s dollars, that original limit from 1970 would equate to roughly $80,000 - meaning the modern CTR casts a far wider net than lawmakers originally intended.

Inside the Proposal: Modernisation or Misstep?

Proposed as the Streamlining Transaction Reporting and Ensuring Anti-Money Laundering Improvements for a New Era Act (STREAMLINE), the legislation aims to update these CTR thresholds to reflect economic reality.

Key elements include:

CTR threshold: Raised from $10,000 to $30,000

SAR threshold: Raised from $5,000 to $10,000

MSB threshold (for money-service businesses): Raised from $2,000 to $3,000

Automatic inflation indexing: Every five years, thresholds would adjust to maintain purchasing-power parity

Proponents argue that these changes would right-size reporting obligations and bring decades-old limits into the 21st century. But the implications reach far beyond a simple numeric change.

The Case for Raising the Threshold: Reducing Noise, Restoring Proportionality

Volume versus value: Banks collectively file millions of CTRs each year - with approximately 20.8 million in 2023 alone, according to FinCEN data[1]. Critics note that this flood of routine filings may obscure genuine criminal activity, rather than highlight it.

Relieving unnecessary compliance strain: While large banks have automated CTR filings, smaller or regional institutions still dedicate significant resources to reporting queues, quality assurance, and customer inquiries.

Improving signal-to-noise ratio for law enforcement: Fewer low-risk transactions mean agencies can concentrate analytical attention on genuinely anomalous behavior.

Future-proofing through indexing: Automatic adjustments would prevent another half-century lag and align with efforts to modernize the U.S. AML framework.

Supporters see the change as pragmatic, not permissive - a recalibration designed to make the AML system smarter, not softer.

The Counterargument: What Could We Be Risking?

Cash is rarer - and therefore riskier: In today’s digital-first economy, dominated by electronic transfers and peer-to-peer payments, large cash movements are increasingly uncommon. Raising the threshold could delay visibility into the very transactions that now stand out most.

The ‘structuring’ blind spot: One of the most effective AML red flags is detecting structuring - when individuals break up deposits to stay below reporting limits. If the CTR threshold triples to $30,000, criminals could move significantly more illicit cash before detection.

Implementation challenges: Even automated systems require reprogramming, training, and procedural revalidation. The one-time operational lift could outweigh short-term relief, especially in diversified institutions.

Law-enforcement uncertainty: While many CTRs may offer limited investigative value, data on their effectiveness remain inconclusive. Without clear feedback loops, raising thresholds risks unintentionally shrinking the evidentiary trail investigators rely on.

In summary, opponents caution that raising the threshold may diminish the early-warning function of cash-reporting, even if the compliance burden appears lighter on paper.

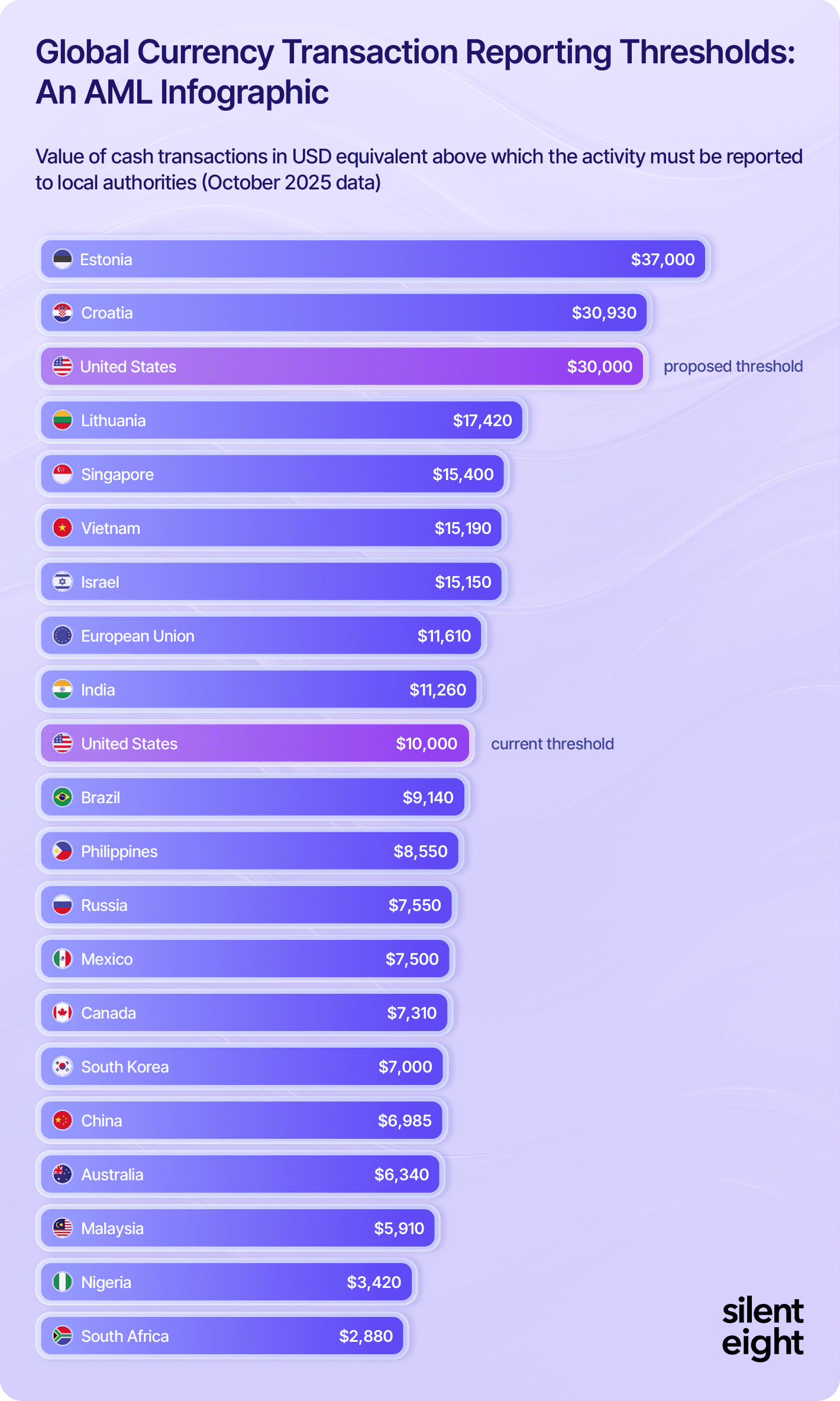

Beyond U.S. Borders: How America’s Threshold Stacks Up Globally

To understand what a $30,000 limit would mean in context, it helps to look abroad. Reporting thresholds vary dramatically across jurisdictions - shaped by differing financial-crime risks, cash-usage patterns, and regulatory philosophies.

If enacted, the U.S. threshold would move from the mid-range globally to near the upper end, comparable to Croatia’s current level. However, direct comparisons can be misleading: some countries set cash-payment caps (bans above a certain value), while others - like the U.S. - rely on post-transaction reporting.

Still, the diversity of global thresholds underscores that there is no universal benchmark for defining a “large” cash transaction. Still, the proposed U.S. limit would place the country toward the higher end of the international spectrum - a notable shift for one of the world’s most scrutinized financial systems.

Shifting the Landscape: Implications for the AML and FCC Industry

Rethinking transaction-monitoring: If thresholds change, firms must adjust not only CTR generation but also the downstream analytics that rely on CTR data - structuring models, peer-group comparisons, and customer-risk segmentation.

Managing institutional change: Policies, procedures, and training materials referencing ‘$10,000’ would require review and approval. Testing and model-validation teams would need to ensure system accuracy before the new limit goes live.

Reallocating compliance resources: Reduced CTR volumes could free up bandwidth for more qualitative investigations, complex case analysis, or enhanced suspicious-activity detection. But firms will need to strike a balance to avoid any perception of relaxed vigilance.

Data and supervisory implications: Regulators and FinCEN may need to recalibrate expectations and analytical models built on decades of $10,000-based reporting data. Historical trend analysis could be disrupted - a non-trivial concern for institutions that rely on longitudinal CTR patterns.

Global consistency challenges: For global banks operating across multiple regions, the U.S. adjustment would add another layer of divergence. Compliance officers will have to ensure consistent group-wide AML standards while adhering to local variations.

Ongoing recalibration: The proposal’s inclusion of automatic inflation adjustments every five years means the CTR and SAR thresholds won’t remain static. While this keeps reporting aligned with real-world values, it also introduces a recurring compliance cycle. Each adjustment will require updates to systems, policies, and training materials, meaning institutions will need to plan for regular, scheduled change rather than a one-off implementation.

Ultimately, the proposal presents both opportunity and operational complexity - a moment for the industry to modernize, but one that demands meticulous execution.

Navigating Change Without Losing Sight of Risk

Whether or not the proposal becomes law, it highlights a broader truth: AML systems must evolve alongside the economies they monitor.

Tools designed for a cash-heavy, paper-driven era now operate in a world of instant payments, digital assets, and AI-assisted compliance. Revising the CTR threshold may be necessary modernization - but modernization must never come at the expense of vigilance.

For compliance leaders, now is the time to:

Review cash-flow and structuring scenarios in transaction-monitoring programmes

Assess potential policy, system, and training updates

Strengthen cross-channel detection for non-cash typologies (digital fraud, crypto, mule networks)Stay informed as legislative debate unfolds

The conversation around CTR thresholds is as much about future-proofing AML frameworks as it is about recalibrating numbers.

Final Thoughts: A Turning Point for U.S. AML Policy

More than 50 years after the Bank Secrecy Act first set the $10,000 benchmark, the U.S. is re-examining what ‘large’ really means.

If executed thoughtfully, the new threshold could sharpen rather than soften the country’s AML defenses - but its success will depend on how intelligently regulators, law enforcement, and financial institutions adapt.

Either way, this moment marks a defining chapter for compliance professionals: one that calls for vigilance, agility, and foresight.

Share article